India’s fast breeder reactor milestone may increase the strategic importance of a small group of domestically qualified nuclear suppliers. The Prototype Fast Breeder Reactor (PFBR) achieved first criticality in April 2026, advancing the second stage of India’s three-stage nuclear programme.

India’s three-stage nuclear programme is designed to eventually utilise the country’s large thorium reserves, which require conversion into fissile material before they can function as reactor fuel. India has limited uranium reserves but holds one of the world’s largest thorium reserves. Thorium itself cannot directly fuel a reactor. It first needs to be converted into fissile material.

In the first stage, conventional pressurised heavy water reactors (PHWR) generate electricity using uranium while producing plutonium as a by-product. The second stage uses fast breeder reactors to convert thorium into uranium-233, which can later function as nuclear fuel. The final stage aims to build a largely indigenous thorium-based nuclear fuel cycle.

It is in this context, that the PFBR milestone becomes critical. Nuclear manufacturing ecosystems differ materially from conventional industrial capex cycles. Reactor-grade pumps, motors, control systems, and reactor assemblies require years of qualification, operational validation, and regulatory approval, limiting the number of suppliers capable of participating in reactor construction and long-duration maintenance programmes.

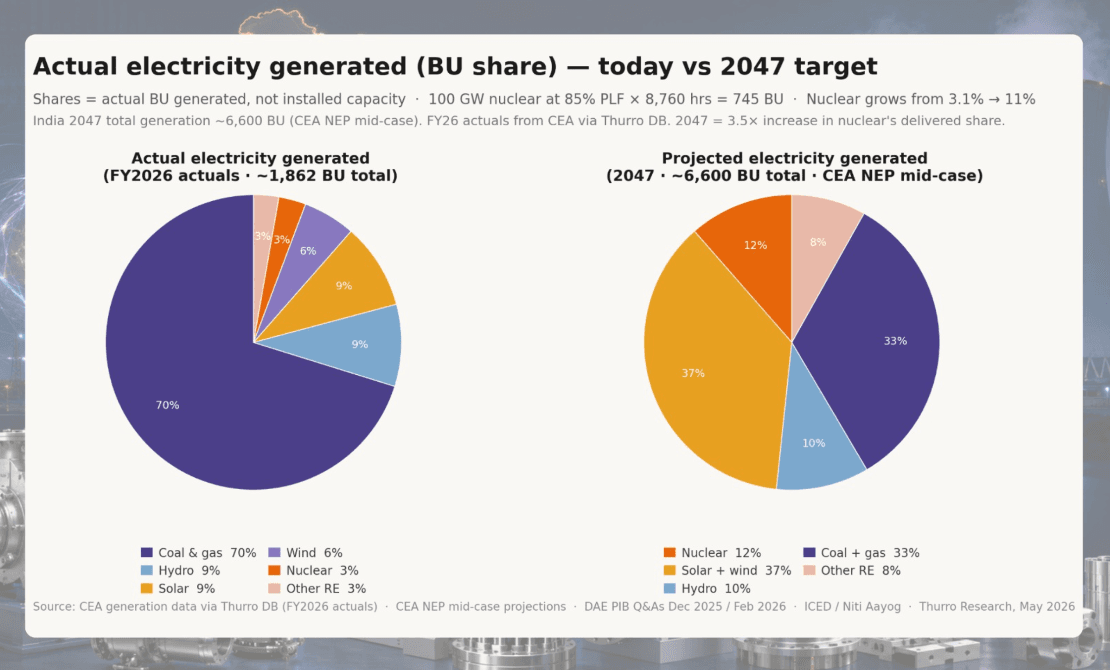

That constraint becomes more relevant as India expands its nuclear ambitions. Nuclear currently accounts for only 1.65% of installed electricity capacity, yet contributes 3.41% of actual electricity generation because reactors operate at significantly higher plant load factors than most other power sources. India’s 100 GW nuclear target by 2047 implies a substantial increase in reactor construction, component replacement cycles, and nuclear-qualified industrial capacity.

As reactor construction scales, qualification itself may function as a competitive moat because supplier substitution in nuclear infrastructure is slow, expensive, and heavily regulated. Three listed companies—KSB, TD Power Systems, and MTAR Technologies illustrate different parts of that ecosystem.

These companies operate across different layers of India’s nuclear manufacturing ecosystem. KSB supplies primary coolant pumps embedded directly into reactor systems, while TD Power Systems manufactures nuclear-qualified motors and electrical equipment, and MTAR Technologies supplies reactor assemblies and control mechanisms used in core reactor operations.

These categories are difficult to commoditise because nuclear infrastructure operates with long asset lives, stringent safety standards, and slow qualification cycles. Once suppliers become integrated into reactor programmes, replacement and requalification costs tend to remain high, limiting supplier substitution and slowing competitive entry.

The screening framework evaluated 23 companies across India’s nuclear supply chain, spanning reactor construction, heavy engineering, turbines, electrical systems, specialty alloys, instrumentation, and ancillary infrastructure. The framework required:

A. exchange-filed evidence of supply relationships with Nuclear Power Corporation of India Limited (NPCIL), which operates India’s commercial nuclear reactors, or Bharatiya Nabhikiya Vidyut Nigam Limited (BHAVINI), which leads the fast breeder reactor programme, establishing actual participation in India’s nuclear reactor ecosystem;

B. nuclear-specific vendor approvals from the Atomic Energy Regulatory Board, which certify technical eligibility to supply reactor-grade equipment through a qualification process that typically takes 7–12 years and involves operational, safety, and reliability validation;

C. financial capacity to absorb long nuclear manufacturing cycles, measured through working-capital intensity, debt levels, interest coverage, liquidity position, and ability to withstand delayed revenue recognition; and

D. management guidance indicating measurable and trackable nuclear growth visibility through investor presentations and earnings calls.

Several prominent companies were excluded despite possessing nuclear exposure. L&T Heavy Engineering and BHEL were eliminated because nuclear revenues were not separately trackable within much larger consolidated order books and management commentary. Walchandnagar Industries possessed strong reactor credentials, but failed financial-strength filters because of negative interest coverage, losses, and ongoing debt restructuring. Other companies including MIDHANI, Engineers India, Thermax, and Kirloskar Brothers were excluded because nuclear exposure remained either indirect, too small to materially influence earnings, or lacked confirmed AERB qualification and exchange-filed NPCIL relationships.

KSB, TD Power Systems, and MTAR Technologies met all four conditions, while also representing different layers of the nuclear manufacturing value chain.

KSB Limited represents the most deeply embedded nuclear manufacturing position within the group. The company has been the sole primary coolant pump supplier for Indian PHWRs since 1982, embedding its products into reactor architecture itself. Nuclear order backlog stood at INR 12.8 billion as of December 2025, representing 49% of total backlog. More importantly, the installed reactor base creates long-duration aftermarket economics. KSB’s nuclear aftermarket order inflows increased from INR 200 million in 2018 to INR 2.3 billion in 2024.

TD Power Systems represents a different type of optionality. Nuclear contributes around 3% of revenue today, but the company is pursuing qualification to supply equipment used inside reactor containment structures after already securing approvals for certain outside-containment nuclear applications from the Atomic Energy Regulatory Board. If obtained, the approval could expand participation into new PHWR construction programmes, thereby increasing its nuclear addressable market.

MTAR Technologies remains the highest nuclear-attribution company within this group. Nuclear accounted for 26.3% of its INR 25.8 billion order book in March 2026. However, the company also carries the highest execution sensitivity.

H1 FY2026 highlighted the company’s execution sensitivity. Nuclear components remained in work-in-progress inventory pending NPCIL inspection and acceptance testing. Total working-capital days increased from 139 in March 2025 to 274 in September 2025, contributing to margin pressure during the period. Nuclear dispatches subsequently accelerated through H2 FY2026 as NPCIL clearances normalised. The sector’s long-term opportunity therefore appears increasingly linked not only to reactor additions, but also to the limited supplier base operating within a slow-moving, qualification-constrained industrial ecosystem.

Thurro does not make buy or sell recommendations on any security. This analysis is based on publicly available data and is intended for informational purposes only. It does not constitute investment advice.

A more detailed version of this analysis, including underlying datasets and extended breakdowns, is available to clients on request. For access, please write to contact@thurro.com.

Cover photo credit: AI generated image

View disclaimer

Unlock the power of alternative data

Do not just follow the market — stay ahead of it. Thurro helps you transform raw filings and alternative datasets into actionable insights.

Explore Thurro AltData Book a demoRelated Articles

How Indian companies navigated the 2026 gas disruption

Companies across chemicals, fertilisers, and ceramics are now reporting curtailed allocations, suspended production lines, and emergency fuel rationing

India’s power demand surge is no longer just a summer story

Electricity consumption data and company commentary suggest India’s summer power demand is becoming structurally broader than residential cooling…

NowCast by Thurro remains disciplined in a tougher quarter

Operational data disruptions widened forecast dispersion in Q4 FY2026, offering a real-world stress test for Thurro’s nowcasting framework.