India’s gas market is no longer dealing with a temporary import disruption. Companies across chemicals, fertilisers, ceramics, and city gas distribution are now reporting curtailed allocations, suspended production lines, and emergency fuel rationing as the continuing disruption at the Strait of Hormuz ripples through the industrial economy.

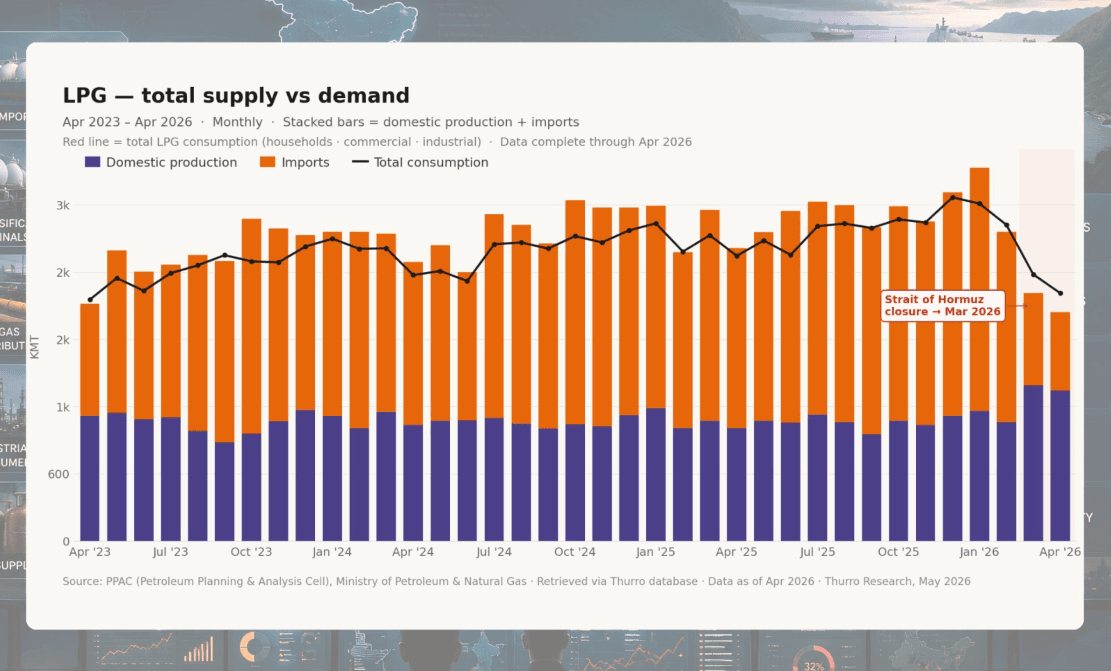

March 2026 was the first month to fully reflect the shock. Liquefied petroleum gas (LPG) imports declined 56.1% month-on-month on a per-day basis. Liquefied natural gas (LNG) imports also weakened. But the sharper signal came from consumption. Per-day natural gas demand fell roughly 20% versus February, while LPG demand dropped around 24%, far beyond normal seasonal movement. Both fuels subsequently showed some recovery in April, but March remains the clearest illustration of the immediate impact of the disruption.

LNG and LPG are distinct fuels despite often being grouped together in energy discussions. LNG is primarily methane cooled into liquid form for long-distance transport and is linked to natural gas infrastructure such as pipelines, regasification terminals, and city gas networks. It is widely used in fertilisers, power generation, industrial fuel systems, piped natural gas (PNG), and compressed natural gas (CNG) networks.

LPG, by contrast, is mainly propane and butane derived during crude oil refining and natural gas processing, and is typically transported in cylinders or pressurised containers. It is widely used in domestic cooking, commercial kitchens, ceramics, glass manufacturing, and several industrial heating applications. The March 2026 disruption affected both fuel systems simultaneously, creating shortages across industrial gas, commercial LPG, and downstream manufacturing.

The data suggests India’s gas market is entering an allocation regime where industrial demand is being suppressed to protect priority consumers. The following management commentary from Q4 FY2026 captures how the disruption spread across LNG imports, city gas distribution, industrial fuel allocation, and downstream manufacturing.

Across sectors, the commentary suggests that the disruption in the Strait of Hormuz evolved from a supply-chain shock into a system of rationed fuel allocation. LNG importers and city gas distributors described abrupt supply curtailments, force majeure conditions, pooled-gas allocation mechanisms, and priority diversion toward domestic PNG, CNG, and fertiliser demand. Industrial users across ceramics, chemicals, fertilisers, glass, and hospitality simultaneously reported curtailed fuel access, higher spot prices, operational disruption, and operational adjustments ranging from production cuts to switching toward alternate fuels and electric induction systems.

Multiple companies also pointed to secondary effects beyond fuel availability itself, including labour displacement in Morbi, ammonia-linked fertiliser inflation, event cancellations in hospitality, and pressure on industrial margins from sharply higher gas procurement costs.

Taken together, the disclosures suggest India’s gas market temporarily shifted away from normal price-led balancing toward managed allocation and demand suppression, with downstream industrial activity increasingly adjusting to constrained LNG and LPG availability.

1. LNG importers / regasification

GAIL (India), Regulation 30 disclosure, March 5

“…due to supply restrictions imposed by PLL, the allocation of LNG quantities to GAIL under the said contract has been reduced to zero with effect from 4th March 2026.

“GAIL is currently assessing the situation with respect to any supply curtailment that may need to be imposed on its downstream customers. Notwithstanding the above, LNG supplies to GAIL from other sources/suppliers are currently unaffected.”

Petronet LNG, Regulation 30 disclosure (Disruption of Operations), March 3

“…vessels are presently unable to safely transit through the Strait of Hormuz to reach Ras Laffan, the loading port of QatarEnergy.

“The Company has issued a Force Majeure Notice to QatarEnergy in respect of its LNG tankers, namely Disha, Raahi, and Aseem… Consequently, the Company has issued corresponding Force Majeure notices to its off-takers, namely GAIL (India) Limited, Indian Oil Corporation Limited (IOCL), and Bharat Petroleum Corporation Limited (BPCL).

“Acts of War is also excluded under Business Interruption Insurance covers taken by Petronet LNG.”

Q4 FY2026 earnings call, May 5

Saurav Mitra (director, finance, and CFO): “…We hope that the situation in the Gulf improves very soon, which is going to have a very positive impact in our operations and as well as on the financials. And we also expect to come out with a brighter picture of the financials of the company when we meet next.”

On utilisation: “the Dahej capacity utilisation during March was around 53% and Kochi was slightly more than 20%.”

2. City gas distribution

Adani Total Gas, Q4 FY2026 earnings call, April 28

Suresh P. Manglani (CEO): “Since late February, geopolitical tensions in West Asia have disrupted global energy markets, resulting in higher natural gas prices, supply chain challenges and compounded currency volatility. Recognizing this, government took several proactive steps like prioritizing supply of pipe natural gas to homes, CNG for transport sector and other key sectors.”

Ravindra Desai (Head of gas sourcing): “…the government decided to help the CGD industry during this crisis. And we have seen that the priority segments like CNG and the domestic has been 100% supplied by the government to the domestic allocation. In addition to that, they appointed GAIL as the nodal agency, and they work very well in tandem with the CGD industry to provide support during this crisis.”

“Global LNG supply shock reduced Mar-26 LNG imports by ~16% YoY, and sharply increased sourcing costs amid LNG supply constraint due to closure of strait of Hormuz led to higher benchmark prices and ~5% INR depreciation…

“Industrial volumes were temporarily curtailed in a calibrated and transparent manner… Gas costs passed through in calibrated manner with an excess gas price introduced for volumes beyond the curtailment threshold.”

Gujarat Gas, Regulation 30 disclosure, April 23

“During the recent geopolitical crisis, the company proactively sourced natural gas from non-Middle East markets at spot rates to maintain continuous supply…

“The crisis led to a surge in raw material costs, restrictions on industrial propane usage, and increased freight expenses, prompting several ceramic units in Morbi to voluntarily suspend operations starting mid-March 2026 thereby affecting livelihood of more than 2 lakh workers…

“Industrial activity in Morbi has gradually resumed in April 2026, with gas consumption increasing from approximately 0.36 mmscmd (serving around 83 units) as of 31st March, 2026 to approximately 2.70 mmscmd (serving around 290 units) as of 22nd April, 2026.”

IRM Energy, Q4 FY2026 earnings call, May 9

M.K. Sharma (CEO): “…in the last quarter, you know, suddenly the APM allocation was impacted. Then NWG prices which is formula-based, that also started coming a little higher, and there was a, I mean, challenge in the industrial segment for the gas availability part of it also…

“Rather we are adding more customers in the commercial segment, hotels and other commercial areas who were using LPG earlier. They are now aggressively reaching us out.”

Mahanagar Gas, Q4 FY2026 earnings call, May 8

Rajesh Patel (CFO): “…100% of the domestic PNG is through APM, which is locally produced. And as far as CNG is concerned, majority is out of domestically produced and balance was assured through pooled gas mechanism, which was announced somewhere around 9th of March.

“As far as industrial and commercial customer category has been concerned, roughly 80% supply was maintained, curtailing around 20%, within which probably from time-to-time directives have changed to ensure that small commercial restaurants, schools, colleges, crematorium, etc, should be supplied 100%.”

Rajesh Wagle (Senior vice-president, marketing): “Overall, in the month of March, we lost about 1.25 lakh, 1.3 lakh scmd out of, let’s say, Feb average of 5.75. About 20%, 22% volume we lost… Commercial, we managed to maintain supplies because many of them were going to critical customers, hospitals, canteens, messes of government institutions, schools, etcetera. It was a large industry where the supply was curtailed a bit.”

3. Ceramics & sanitaryware

Cera Sanitaryware, Q4 FY2026 earnings call, May 14

Deepak Chaudhary (vice-president, finance): “In case of sanitaryware, the clay etcetera. has increased, but the bulk of the price impact comes in on account of gas. Like most of the players in the Morbi have been severely impacted because of the rise in the kind of prices which have happened in the prices of gas. And also in the month, in the coming quarter, we expect that even though Morbi plants have started opening up… even though while they have started opening up, most of the labour would have gone back home at the time when the plants were closed. And it will be a gradual process by which the labour would come in, and the plant plants will start opening.

Kajaria Ceramics, Q4 FY2026 earnings call, April 30

Ashok Kajaria (chairman): “Government of India has issued a circular on 5th of March that propane will not be supplied to industry. It will only be used for domestic LPG production. No industry is getting propane for your information…

“Government’s first priority is to give LPG to domestic, number one… Second priority is to give to fertilizer because that’s an area they can’t afford to this thing… Third priority, as you know earlier, was power. Industry was coming later. They are not giving any gas to the power industry. They say no, I can’t give you gas. Industry has been put on a priority number 3.”

On the gas-pool formula: “Government of India has set a certain formula. They have made GAIL as a nodal agency on 9th of March that you will coordinate for the entire gas pipeline because of this war.

“Now what they have done as per government guideline, whatever you have lifted in the last 6 months, you will get — they started out with 80% at normal prices, 20% at spot prices. Got reduced to 65%, then to 55%. Again, raised to 65% and again to 80%.”

Sanjeev Agarwal (CFO, on gas prices): “North is roughly INR55.54 per SCM for quarter 4. South was INR49.6 and West was INR46.57… April, the price in North is roughly INR62.5. South is around INR81 and West is INR79.”

Chetan Kajaria (vice chairman): “…we have taken a price increase of roughly 12% to 13% in our North plants and Morbi has been slightly higher around 16% to 17% because the gas price has gone up much higher there.”

4. Fertilisers & chemicals

Gujarat Narmada Valley Fertilizers & Chemicals, Regulation 30 disclosure, March 6

“Due to the supply constraints, the allocation of RLNG quantities to GNFC under the Supply Agreement has been restricted to 60% of the Daily Contracted Quantity (DCQ) on an overall basis with effect from March 06, 2026. This will have an impact on the production of Neem Urea.”

Q4 FY2026 investor presentation, May 18

“Availability of feedstock had been an issue for some time in March-26 due to war situation…

“Spike in chemical prices has led to better realization due to geo political situation which improved the margin profile…

“Company served the industry need, both, for ammonium nitrate and technical grade urea in view of shortages.”

Madhya Bharat Agro Products, Q4 FY2026 earnings call, April 20

Pankaj Ostwal (managing director): “There are three key nutrients N, P and K, where nitrogen comes from ammonia, which in turn is derived from natural gas. Since India imports natural gas, any impact on global oil and gas prices ultimately affects ammonia costs. Accordingly, ammonia prices have increased due to higher natural gas prices, with the impact f lowing through from Middle East markets.”

“Ammonia prices have gone up by, it has gone up by almost ₹ 45,000/MT.”

Pukhraj Kanther (group financial advisor): “And we have increased our MRP by 50%.”

Pankaj Ostwal (on industry): “The fertilizer sector is currently navigating a period of unstable and supply chain disruption arising from geopolitical disturbances in West Asia. This has led to a direct impact on the escalation of raw material input costs that include natural gas and ammonia apart from others… Sulphur, which is a key input for SSP and phosphoric acid, saw a sharp increase during FY26, moving from $100 MT in FY24 to almost $700 MT.”

Meghmani Organics, Q4 FY2026 earnings call, May 16

Ankit Patel (chairman and managing director): “In current geopolitical situation where we see the overall cost has gone up, one of the biggest impact is on the Fertilizer segment because Fertilizer is linked to the ammonia and ammonia is linked to the natural gas. So globally there has been a significant increase in the cost of fertilizers…

“So on the ground level, there has been a lot of work going on by the government where they are calling the senior distributors and dealers and informing that there is going to be the fertilizer shortage. So rationalize it and pass on the matter to the farmer level and try to promote other products than Urea and DAP.”

Tata Chemicals, Q4 FY2026 earnings call, May 4

R. Mukundan (managing director and CEO): “…there has been a notification on ammonia… the fertilizer units have been advised not to supply to non-fertilizer users. We’ve written to government that this order is going to impact all of us. As of now, we are fine, but we’re closely monitoring it and we are also sure government will look into this. It is about 1% of the entire ammonia consumption in the country.”

5. Solar glass

Borosil Renewables, Q4 FY2026 investor presentation, May 12

“Due to the ongoing war in west Asia the price of imported LNG has more than doubled. In this difficult situation, the company had no choice but to request customers to accept a fuel surcharge covering a part of the cost increase which they accepted. We did not curtail production and have been able to maintain full production throughout. Looking to this adverse situation, the company has further intensified efforts to improve efficiencies and cut costs. As a result, the rise in fuel cost has not made any impact on our margins.”

6. Hospitality

Brigade Hotel Ventures, Q4 FY2026 earnings call, April 29

Rayan Aranha (vice-president): “…4 of our hotels are, you know, they run on PNG and the rest are LPG dependent. But however, considering the scope of kitchen operations across the hotel, there is a large amount of electric induction also available which we move to very quickly. So we didn’t really see a lapse as such. There was no hotel which ran out of a gas supply. While there was reduced supply coming in from the CNG line, we still managed to supply the food that we had to.”

Manoj Agarwal (COO): “…because of these disruptions during the last month of March and some bit of it still continuing, we faced a few cancellations on account of larger events… We manage to restructure our or redefine our menus and take in alternative items in the menu… we switched to inductions now in many of our hotels.”

Kamat Hotels, Q4 FY2026 earnings call, May 16

Vishal Kamat (executive director): “…new project executions would be challenging because of material supply availability today because of LPG. It’s not only hospitality, but real estate and even simple office renovation, home renovation, any kind of utility for materials because of the tiles being a big challenge because LPG is required for tile manufacturing.”

Indian Hotels Company, Investor Presentation Q4 FY2026, May 11

“Q4 IMPACTED BY TEMPORARY GLOBAL DISRUPTIONS…

“Managed LPG Supply Disruptions through use of alternative fuels in domestic hotels… March powered by Domestic tourism yet impacted adversely by ₹ 40-45 Crores at Consol level.”

The analysis reflects company commentary and disclosures rather than an independent assessment of geopolitical developments.

Cover photo credit: AI generated image

View disclaimer

Unlock the power of alternative data

Do not just follow the market — stay ahead of it. Thurro helps you transform raw filings and alternative datasets into actionable insights.

Explore Thurro AltData Book a demoRelated Articles

India’s nuclear push is creating a scarcity premium for certified suppliers

India’s thorium strategy and fast breeder reactor progress could reshape the economics of India’s nuclear manufacturing ecosystem

India’s power demand surge is no longer just a summer story

Electricity consumption data and company commentary suggest India’s summer power demand is becoming structurally broader than residential cooling…

NowCast by Thurro remains disciplined in a tougher quarter

Operational data disruptions widened forecast dispersion in Q4 FY2026, offering a real-world stress test for Thurro’s nowcasting framework.