Trends and transformations in India’s tractor industry

JULY 2025

By Akhilesh Tilotia

Key insights

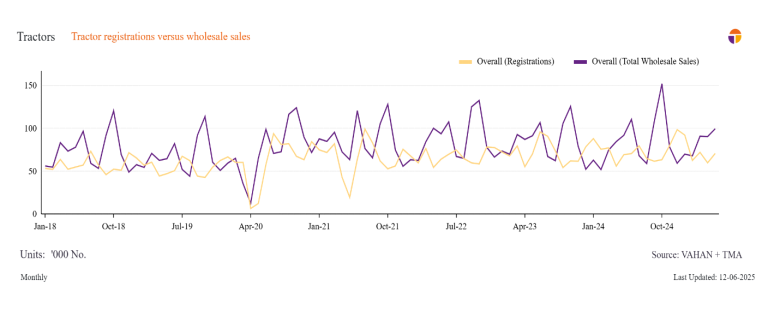

India produces one-third of the world’s tractors, yet reliable data on sales and demand remains split across two key sources: The Tractor Manufacturers Association (TMA) and Vahan. TMA data reflects wholesale sales (manufacturer to dealer) while Vahan data captures registrations, a closer proxy for retail demand. In recent years, registrations have grown faster than wholesale sales, which may reflect improved market access and more effective registration practices.

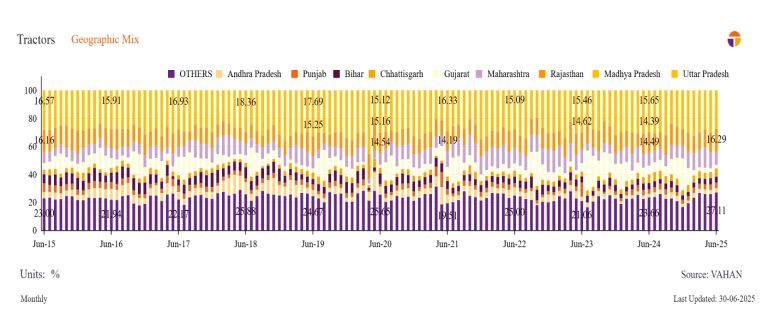

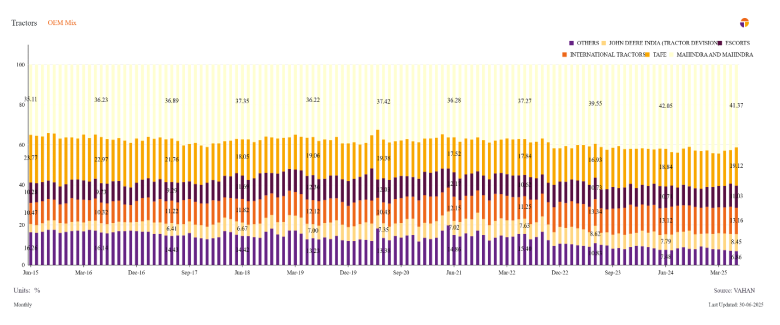

Granularity in Vahan data helps us to get deeper into location and brand market shares. Over the past decade (FY2016-FY2025), five states (Uttar Pradesh, Rajasthan, Madhya Pradesh, Maharashtra, and Gujarat) have consistently contributed 58–61% of all registrations. Mahindra & Mahindra has led the market with a 36–43% share, and together with TAFE, Sonalika, Escorts, and John Deere, these top five brands have made up 85–90% of all registrations.

The two data approaches: TMA versus Vahan

The Indian tractor industry has emerged as the largest in the world, accounting for about one-third of total global tractor production. Two major data sources attempt to depict this market: the Tractor Manufacturers Association (TMA) and Vahan, a government-operated vehicle registration database maintained by the Ministry of Road Transport and Highways.

While both datasets are complementary and publicly available, they represent two distinct approaches to tracking India’s tractor market. TMA aggregates wholesale sales (manufacturer to dealer) figures directly reported by manufacturers, while Vahan compiles registration data from Regional Transport Offices (RTOs) nationwide. A key advantage of Vahan is its granularity – It represents detailed information about each vehicle, including type of vehicle, model, fuel type, registration, and even registration timing, allowing more sophisticated analysis of market trends.

Thurro collects Vahan data daily. This allows us to update clients with the latest retail trends. Given our decade-long dataset from Vahan, we apply statistical analysis to extrapolate the current month’s sales to offer a real-time view.

Registration data gains ground as a more accurate measure of retail tractor demand

Over FY2019 to FY2025, wholesale tractor sales, as reported by TMA, saw a compounded annual growth rate (CAGR) of 3% per year, while registrations, as reported by Vahan, increased at a CAGR of 4.8%. The higher growth rate in registrations compared to wholesale sales could be due to more tractors reaching customers, the clearing of previously accumulated inventory, or enhancements in how registrations are processed.

The data shows clear seasonality. Wholesale sales typically peak in June and October when original equipment manufacturers (OEMs) send inventory to their dealers. Registrations peak in

July and December, coinciding with the Kharif and Rabi cropping cycle. The lowest activity is usually seen in August and December for wholesale sales, while registrations dip in August and October. The consistent peaks and troughs highlight a 1–2-month lag between wholesale sales and registrations. This can be explained by manufacturers often building inventory at dealerships ahead of anticipated demand. This dynamic reinforces the view that registrations, as reported by Vahan, serve as a more accurate proxy for consumer demand.

Over the last seven years (FY2019-2025), the share of registrations tracked by Vahan compared to wholesale sales hovered around 75% until FY23. It jumped to over 90% in FY2024 before settling at nearly 84% in FY2025. We note that Vahan will never reach 100% as Telangana and Lakshadweep registrations are not reported via Vahan. This rising share indicates that Vahan data is increasingly beginning to reflect the underlying market dynamics.

| Wholesale sales (‘000) | Registrations (‘000) | Registrations-sales ratio (%) | |

| FY2019 | 872 | 654 | 75 |

| FY2020 | 781 | 639 | 81.9 |

| FY2021 | 988 | 743 | 75.2 |

| FY2022 | 971 | 725 | 74.7 |

| FY2023 | 1,070 | 802 | 74.9 |

| FY2024 | 965 | 881 | 91.3 |

| FY2025 | 1,039 | 870 | 83.8 |

What does Vahan data reveal: Top 5 states in registrations account for 56-61% of tractor registrations

Uttar Pradesh has maintained its position as the leading state, with approximately 16.5-17.3% market share in registrations between FY2016 and FY2025, followed closely by Rajasthan (12.9-13.7%) and Madhya Pradesh (10.9-13.2%). Meanwhile, Maharashtra and Gujarat saw largely consistent increases in the last decade; Maharashtra’s share climbed from 7.5% to 10% and Gujarat’s from 7% to 9.1% in the past decade. Cumulatively, these five states have consistently accounted for more than half of the total market share over the last ten years.

Gujarat, in particular, stood out with a record 13.1% share in FY2024. This surge was likely driven by policy efforts such as the Atal Bhujal Yojana in FY2023, aimed at improving groundwater management in water-stressed regions. These measures provided a strong push to tractor demand, as noted in M&M’s FY2024 annual report. While registrations and market share in Gujarat declined in FY2025 due to a high base effect, volumes remained robust – 28% higher than FY2023 levels.

Bihar experienced the sharpest decline, losing 330 basis points as its market share fell from 7.3% to 4%. Andhra Pradesh also faced a drastic decline, dropping from 6% in FY2017 to a low of 0.6% in FY2021 before recovering to 2.9% by FY2025. At the same time, the market has gradually shifted towards regions that were previously underpenetrated. Chhattisgarh, for example, has increased its share from 3.5% to 5.1%, now ranking among the top ten states for tractor registrations.

Stable industry with top 5 players accounting for 85-90% market share

Mahindra & Mahindra (M&M) maintained its strong position with market share rising consistently from 36.8% in FY2016 to 42.9% during FY2025. TAFE, which has consistently held the second position in market share, ceded 590 basis points from 23.9% in FY2016 to 18% in FY2025. International Tractors Limited (part of the Sonalika Group) maintained a steady third position with approximately 11.3-13.2% market share. Escorts remained fourth with a stable 10% market share during the last decade. John Deere, in fifth position, saw its market share rising steadily from 4.6% to 7.8%.

From low to higher horsepower (HP) and back

Over the past decade, the Indian tractor industry has shifted from being dominated by low-powered models (below 30 HP) to a greater share of medium and higher horsepower tractors. This shift has been driven by shrinking average landholdings and a decline in rural labor

availability, as highlighted in the Economic Survey 2017–18. Farmers are seeking more efficient machinery to improve productivity under these changing conditions.

Our analysis on Regional Transport Offices (RTOs) in Telangana reveals that low HP tractors saw a sharp decline at a CAGR of 8.7% between FY2020 and FY2025. Conversely, the medium HP segment (30–50 HP) and the high HP segment (above 50 HP) experienced robust growth, rising by nearly at a CAGR of 14.3% and 8.1%, respectively, over the same period. Importantly, the weighted average horsepower has remained stable across all tractors, rising from 37 HP in FY2020 to 40 HP by FY2025. This marks the medium HP segment as a clear market anchor.

However, the 2023 revision of Tractor Emission Regulations-Stage IV (TREM-IV) emission norms for tractors above 50 HP has made higher HP tractors more expensive, nudging demand back to the medium segment. In response, companies have realigned their product portfolios, introducing new models and upgrading existing ones to suit evolving demand.

Exports value growth outpaces volume

Between FY2019 and FY2025, Indian tractor export volumes, as reported by TMA, grew at a muted CAGR of just 1.2%. In contrast, export values, as reported by the Department of Commerce, saw a faster CAGR of 11.9% during the same period. Values surged from Rs 62 billion in FY21, reaching a peak of Rs 119.7 billion in FY23 before declining to Rs 92 billion in FY2024. Encouragingly, FY25 has seen a recovery in export values, with monthly figures slightly exceeding Rs 93 billion.

The disparity between volume and value growth suggests that Indian tractor exports are benefiting from higher average prices, potentially driven by a greater share of high-horsepower models in the export mix. Government policies, such as the Agriculture Export Policy and Production Linked Incentive (PLI) schemes, may have supported the global competitiveness of Indian tractors, though their precise impact is difficult to isolate.

Thurro’s detailed monthly tracking of import and export data, including destination countries using granular eight-digit HS codes, provides further insight. The United States is currently India’s largest export market for tractors, accounting for 21.4% of total exports in the last 12 months. Brazil (7.9%) and Mexico (6.6%) follow, underscoring India’s strong presence in both North and South America. This expanding export footprint highlights the growing global relevance of the Indian tractor industry.

Disclaimer

By using the information in this document and on Thurro platforms, you implicitly agree to the following terms of use:

ADQvest (Company) shall not be liable or responsible for any errors in data other than vouching for the arithmetical accuracy of the operations performed by it on the original data.

While every effort is made to ensure data quality, data is provided “as isˮ. The burden of fitness of data lies with the user. The accuracy of the userʼs statistical analysis and any reported findings are not the responsibility of ADQvest. Nothing arising from the data should be taken to constitute professional advice or a formal recommendation.

There can be no assurance that any estimates or underlying assumptions will be realized and that actual results of operations or future events will not be materially different from the estimates. Under no circumstances should the inclusion of the estimates be regarded as a representation, undertaking, warranty or prediction by the company.

In no event shall Company be liable for any incidental, indirect, consequential or special damages of any kind, or any damages whatsoever, including, without limitation, those resulting from loss of profit, loss of contracts, goodwill, or business relationships arising out of or in connection with the use of our data.

Users shall refrain from distributing or selling the data sets to any other individual, institution, or organization without the written consent of the company.

You agree to indemnify, defend and hold harmless the company from and against any claim, action or demand, including, without limitation, reasonable legal fees, made by any third party against the due to or arising out of your use of our content.